International tax planning - The Dutch Finance Company

The Dutch finance company is a frequently used and reliable tax planning instrument. There are many companies in The Netherlands which main activity is to provide loans to group companies.

Historically speaking, the main reason for using The Netherlands as the location for a group finance company is the favourable Dutch tax regime for flow through financing activities (tax ruling for financing activities) and the excellent legal and financial infrastructure.

Per today this is still the case, but also a new regime for group financing activities is introduced; as from 1 January 2010 income from qualifying group financing activities qualifies for a special tax treatment which results in an effective tax rate of five percent (5%). For more information please look at our news item on this subject.

We emphasize that if the new legislation will actually enter into force, The Netherlands will instantly become the most tax efficient regime for group financing activities within the European Union !

We have extensive knowledge and expertise in the area of Dutch finance companies and we are gladly prepared to advice you further on this subject or guide you to other professionals who can help you in other specialized areas (like international lawyers, accountants or trust companies).

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

The activities of a Dutch finance company

The activities of a Dutch finance company primarily consist of providing loans to group companies, subsidiaries, sister companies or shareholders.

There are virtually no limitations with regard to the activities of a Dutch finance company. It can also have a role with the hedging of financial risks of the group and other treasury activities.

The finance activities can be combined with holding activities, royalty activities or actual operating activities, like trading or manufacturing.

The centralization of activities in a Dutch finance company will make the structure as a whole more robust and resistant to the international tendency to deny tax advantages to purely tax driven vehicles. We refer also to the page The Dutch holding company plus.

The activities of the finance company can differ depending on the purpose of the structure. Roughly speaking one can distinguish the new Dutch group finance company (as from 2007), the Dutch conduit company, the Dutch fund raising vehicle and the Dutch group finance branch company.

We have extensive knowledge and expertise with setting up group finance companies on behalf of foreign and domestic clients and we are gladly prepared to advice you further on this subject.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

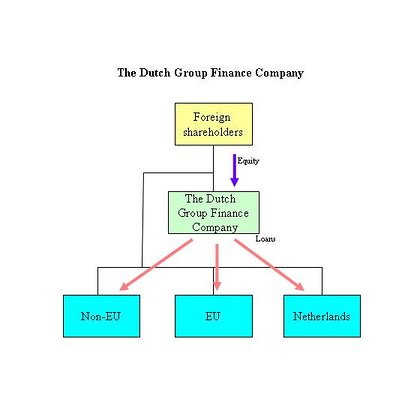

The Dutch group finance company (presumably as from 2010)

As from 1 January 2007 Dutch tax law provides for a special regime for qualifying group financing activities.

Where it comes down to is that the net interest income realised by the tax payer with qualifying group financing activities is subjected to an effective Dutch tax rate of 5%. The normal statutory rate applies, but effectively 80% of the net interest income is excluded from the taxable base.

Special rules are to be provided for the calculation of tax credits for foreign withholding taxes incurred.

We emphasize that on 8 July 2009 the European Commission approved of this new regime and teh Dutch legislator announced that they will issue a bill of law for the intrt5oduction of teh so-called "Group Interest Box Regime" shortly. The expected entry into force is 2010. For more information please look at our news item on this subject.

We have extensive knowledge and expertise with setting up group finance companies on behalf of foreign clients and we are gladly prepared to advice you further on this subject.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

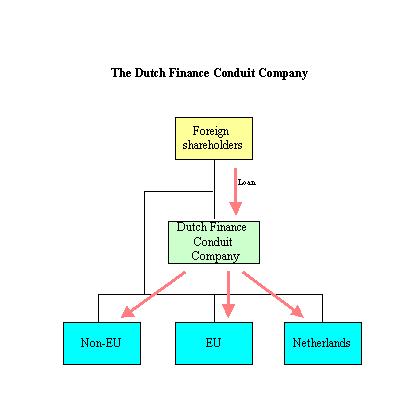

The activity of the Dutch conduit company consists of borrowing money from a group company and lending it on to another group company. The Dutch company then functions as a conduit for providing loans within the same group of companies.

The primary motive for this structure is in many cases the reduction of foreign withholding taxes.

The Dutch fund raising vehicle

The Dutch fund raising company allows easy access to the Dutch and/or the international financial markets. Instead of borrowing money from group companies, the Dutch company takes up loans in the market place on behalf of the group or specific group companies. It can do so though a listing at a recognized exchange or on teh secondary market. Main reason for using a Dutch company is that in many cases the cost of funding via a Dutch company is much lower compared to the cost of funding in the home market. Also, the lack of a Dutch withholding tax on interest paid to the loan providers is a strong benefit.

The Dutch company has easy access to the Dutch financial markets and has proven to be an excellent fund raising vehicle. Usually the group will have to provide a collateral or guarantees so that the Dutch company is more than an empty shell.

The primary motive for this structure is fund raising in the market place. The lack of a Dutch withholding tax on interest paid to the loan providers is a strong benefit.

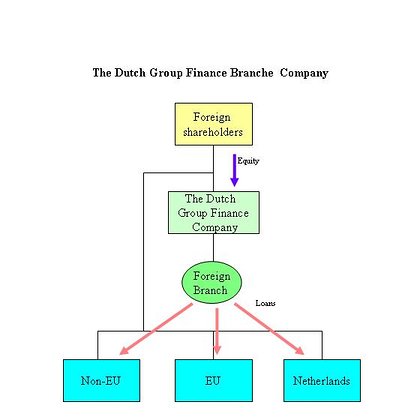

The Dutch group finance branch company

A Dutch group finance branch company in essence functions as the bank of the group or a part of the group.

The treasury activities and the financing of group companies are centralized within the Dutch company. As the Netherlands did until 2007 not have a special tax regime for these kind of activities it was required to involve a second jurisdiction which applies a lower tax rate for group financing activities.

This structure will only be effective if part of the activities are actually carried out in that other jurisdiction. In practice, Luxembourg or Switzerland are frequently used as the second jurisdiction, but technically it can be every jurisdiction (treaty country or non-treaty country) which has a favourable tax regime for financing activities.

The primary motive for this structure is usually the tax efficient funding of subsidiaries. The tax deduction of the interest at subsidiary level and the resulting tax saving is a crucial factor.

It is noted that as a consequence of the introduction of a new Dutch tax regime for group finance activities as from 1 January 2007 the finance branch company has become a relatively less attractive instrument.

The Dutch tax treatment of a finance company

The Netherlands do not have a special tax rate for finance companies. The normal corporate income tax rate applies.

However, since 1 January 2007, the law provides for a special regime for qualifying group financing activities which can result in an effectieve tax rate of 5%.

We have extensive knowledge and expertise with setting up group finance companies on behalf of foreign clients and we are gladly prepared to advice you on this subject.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

The benefits of a Dutch finance company

The benefits of a Dutch finance company depend on the nature of the structure.

In general terms, the main benefits are:

- Low effective corporate income tax rate of 5%.

- The low, or even zero, foreign withholding taxes on interest by virtue of the Dutch tax treaties or the EU-Directive for interest and royalties

- No Dutch withholding tax on outbound interest payments

- No tax haven status for the application of foreign anti-abuse provisions

- No tax haven status for the announced anti-tax haven measures in the US

- The possibility to obtain an advance tax ruling for financing activities

- Tax credits for foreign withholding taxes incurred

- No transfer tax or stamp duties

- No foreign currency exchange restrictions

- The possibility of calculating tax profits in foreign currency (functional currency)

- Effectively no thin capitalization provisions are applicable

- The tax exemption for foreign branch profits

- The possibility to combine activities

The reduction of foreign withholding taxes on interest by virtue of tax treaties

In many countries interest payments made to a debtor in another country are subject to a withholding tax at source. This tax is generally for the account of the recipient (i.e. the Dutch finance company).

Countries are free to determine their domestic withholding tax rates. In practice the withholding tax rate for interest payments is around 30%.

The Netherlands concluded numerous bilateral tax treaties in which the country of origin has only a limited right to levy a withholding tax on interest payments to a Dutch company. For an overview of the treaty rates we refer to the page Dutch treaty interest withholding tax rates.

In order to qualify for the reduced treaty rate most tax treaties prescribe a procedure for an (partial) exemption of the withholding tax at source.

The recipient of the interest (i.e. the Dutch company) must apply for a so-called residence statement with its local Dutch tax inspector. In this statement the tax inspector should confirm that the Dutch company is a tax resident of the Netherlands and, if standard forms are to be used, that it is the beneficial owner of the interest.

In many cases, depending on the applicable tax treaty, a standard form is to be used for this application. The tax inspector will verify the information provided and if he approves the tax inspector will issue a residence statement. This residence statement is then to be forwarded to the payee of the interest who in most cases (depending on local provisions) is then allowed to apply the (partial) exemption of the withholding tax at source.

Nowadays the Dutch tax authorities have become more critical in providing a residency statement. If the Dutch company has no substance in The Netherlands and it incurs no risks on the finance activities, the Dutch authorities may deny the issuance of a residence statement (because the Dutch company is considered not to be the beneficial owner of the interest). This problem should be viewed in conjunction with the current tax ruling policy for flow-through group financing activities.

As from the tax year 2004 the EU Directive for interest and royalties entered into force.

On the basis of this Directive a 0% withholding tax rate applies for qualifying interest payments (or royalties payments) between qualifying associated corporations established in the EU. A corporation is considered associated if it has cross holdings of at least 25% or a third corporation has a direct minimum holding of 25% in two other EU corporations.

The conditions to be met for this EU exemption are:

-

- the beneficial owner of the interest is a qualifying corporation of another EU Member State or is a EU permanent establishment of such a corporation (a corporation as listed in the Annex to the Directive)

- is considered to be a resident in that Member State (and thus not outside the EU)

- and is, without exemptions, subject to tax in that Member State

Dutch withholding tax on interest

The Netherlands do not levy a withholding tax on outbound interest payments.

However, in certain specific cases interest payments may become subject to Dutch dividend withholding tax or to Dutch income tax.

Dutch dividend withholding tax can become due over interest payments if, briefly summarized:

-

- the interest is paid on a loan which according to the Dutch definition qualifies as a profit sharing loan (until 1 January 2007), or

- the interest exceeds normal market rates (constructive dividend), or

- the interest is paid on a loan which for Dutch tax purposes is qualified as capital (deemed capital, constructive dividend - certain profit participating loans after 1 January 2007).

Dutch income tax can become due over interest payments if, briefly summarized,

- the interest is paid to a private shareholder who is deemed to own directly or indirectly "a substantial interest" in the Dutch company, or

- the interest is paid to a corporate shareholder who is deemed to own directly or indirectly a "substantial interest" in the Dutch company and who cannot allocate the loan on which the interest is paid to the equity of an active enterprise.

We have extensive knowledge and expertise with regard to withholding tax issues for foreign-based and domestic clients and we are gladly prepared to advice you on this subject.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

Foreign anti-abuse legislation

One of the reasons to use a group finance company may be to create maximum interest expenses in group companies which are established in high tax countries. It is in particular for this reason, that nowadays many high tax countries only allow interest deduction on group loans within certain limitations (‘thin capitalization rules").

Over the last decade the international community has also become increasingly aware of the phenomenon of treaty shopping i.e. the use of conduit companies with the main purpose to benefit from the reduced withholding tax rates provided by tax treaties. Many countries have incorporated anti-abuse provisions in either their domestic tax legislation or in the tax treaties concluded with other countries, like The Netherlands, to counter the use of purely tax driven conduit companies.

The principles of the new Dutch ruling policy, make the Dutch company quite resistant to foreign anti-abuse provisions, but it should still be verified case by case to what extent a Dutch finance company can be affected by foreign anti-abuse provisions.

Advance tax ruling for Dutch group financing companies

The Netherlands have extensive policy which describes the conditions for obtaining a tax ruling for intra-group financing activities.

The benefit of a tax ruling is that 100% certainty can be obtained with regard to the margins to be reported as taxable profits (transfer pricing) and the right to obtain a residence statement. A resident statement is generally required to invoke treaty benefits (i.e. the reduction of foreign withholding tax rates).

Up to March 2001 it was possible to obtain an advance tax ruling in which fixed margins were agreed upon for virtually risk free finance transactions. As from April 2001 however, new Dutch ruling policy was introduced with far more stringent conditions. The old ruling companies were protected by a grandfather rule which expired in 2005, so that currently all finance companies in The Netherlands need to comply to the new ruling policy.

Under the "new" ruling policy a Dutch finance company must comply with certain operational substance requirements (own office, own bank account, etc.) and economical substance requirements (risks incurred with the finance transactions). The Dutch company should also have an equity at risk of at least 1% of the outstanding loans, or if this is less € 2,000,000. The required equity at risk is dependent on the level of risk incurred on outstanding loans.

The new policy does not provide fixed margins, but instead the taxpayer must provide evidence that the rates used are at arm’s length.

The introduction of the substance requirements in conjunction with the open transfer pricing discussion about the interest rates, have made the process of obtaining an advance tax ruling more burdensome for the tax payer. Rulings are still issued, but the process to obtain it requires more time and effort from the taxpayer.

Nevertheless, the new Dutch ruling policy is generally viewed as an improvement, because the relatively heavy substance of the Dutch finance company and the transfer pricing requirements, make the Dutch finance company more compatible with foreign tax regimes and also more resistant to the anti-abuse provisions of foreign states.

We have extensive knowledge and expertise with regard to obtaining advance tax rulings for finance companies on behalf of foreign clients and we are gladly prepared to advice you on this subject or to represent you in the ruling process.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

Tax credits for foreign withholding tax on interest

If the Dutch finance company incurs foreign withholding taxes on interest received out of another state it will in most cases be entitled to a tax credit.

The Dutch finance company must include the grossed up interest income in its taxable profits (adding back the foreign withholding tax). Without further provisions double taxation would occur because the interest received was already subject to a foreign withholding tax.

As a method to avoid double taxation, the Dutch company is in most cases allowed to deduct the foreign withholding tax from the Dutch corporate tax calculated over the grossed-up interest income (so after adding back the foreign withholding tax). The credit has two limitations. In the first place the credit can never be more than the actual foreign withholding tax paid (unless there is a tax sparing paragraph in the treaty). In the second place the amount of the credit is limited to the Dutch corporate income tax which actually becomes due over the net amount of interest income (after deduction of allocable expenses).

In case the credit cannot be fully utilized in a particular year due to Dutch tax losses, a carry forward is allowed to later years.

The right to a tax credit is usually based on a tax treaty. If for instance a Dutch company incurs Italian withholding tax with regard to interest received out of Italy, the tax treaty between The Netherlands and Italy provides for the entitlement to a tax credit.

If no tax treaty applies (i.e. the interest comes out of a non-treaty state) the Dutch company can nevertheless be entitled to a tax credit on the basis of Dutch unilateral provisions. It is noted however, that this only applies to interest paid out of countries which in the view of the Dutch government qualify as developing countries (and are appointed as such).

The Dutch company always has the choice to abandon its right on a tax credit and instead report the amount of the foreign withholding tax incurred as a business expense.

It is noted that the Dutch ruling policy for finance companies does not explicitly limit the right to a tax credit. So even if the Dutch company is only taxed for a percentage of the interest income, it is in essence still entitled to a 100% tax credit for foreign withholding taxes incurred.

Dutch stamp duties or transfer taxes

The Netherlands do not levy stamp duties or transfer taxes on ordinary loans.

Dutch foreign currency exchange restrictions

There are no restrictions to bring money into the country or to repatriate funds from the Netherlands. There are however some reporting requirements to the Dutch Central Bank.

A Dutch company is under certain circumstances allowed to keep its books and to calculate its taxable profits in a currency other than the EURO. An election should be made before the foreign currency can be applied as functional currency.

No thin capitalization provisions are applicable

The Netherlands have thin capitalization provisions, but they are not relevant for most finance companies.

In summary, the Dutch thin capitalization provisions provide for a maximum debt/equity ratio of 3:1. However, for determining the amount of debt allowed, the incoming loans which are matched by outgoing loans may be excluded. This means that effectively this thin capitalization provision does not have a material impact on most Dutch group finance companies.

The tax exemption for foreign branch profits

A Dutch BV is in essence subject to Dutch corporate income tax for its worldwide profits.

However, on the basis of tax treaties or, if no tax treaty applies, the Dutch unilateral rules for the avoidance of double taxation, the Dutch BV can be eligible for a tax exemption for certain foreign sources of income.

A Dutch BV with a foreign finance branch can under certain conditions qualify for such an exemption. The conditions for the exemption depend on the applicable tax treaty.

If a tax treaty applies:

, the conditions for the exemption can be summarized as follows:

-

- the foreign branch must have substance in the country where it is established (own office, employees, etc)

- the foreign branch must actually conduct business activities (other than managing portfolio investments)

If no tax treaty applies:

, the conditions for the exemption can be summarized as follows:

-

- the foreign branch must have substance in the country where it is established (own office, employees, etc)

- the foreign branch must actually conduct business activities (other than managing port folio investments)

- the financing activities should comply to certain extra (substance) requirements specified in Dutch tax law

- the profits of the branch must actually be subject to a profit tax in the country where the branch is established

The extra substance requirements mentioned under 3, relate to a variety of specified substance requirements. The most important requirement relates to the skills, experience and responsibilities of the employee(s).

If these extra requirements cannot be met, the exemption is replaced by a tax credit for taxes actually paid abroad. It is noted that certain new Dutch tax treaties contain a similar provision.

We have extensive knowledge and expertise with setting up and maintaining finance branch structures on behalf of foreign clients and we are gladly prepared to advice you on this subject.

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

In essence a Dutch finance company is subject to the normal Dutch VAT regime. This means that it should register as a VAT entrepreneur and file VAT returns periodically.

This does however not mean that the Dutch finance company will also actually become subject to the Dutch VAT and be entitled to 100% VAT relief.

To the extent the activities of the Dutch company consist of financial services (like providing loans) it is entitled to an exemption of the VAT. This means that the Dutch company does not need to charge VAT on the remuneration received (like interest).

At the same time however, the relief of input VAT is limited. To the extent total turnover consist of VAT exempt income, no refund of input VAT is allowed, with the exception of input VAT which can be allocated to income from loans provided to non-EU parties.

A Dutch finance company needs to comply with Dutch tax filing and registration requirements.

In essence they are the same as for a normal BV, but as a consequence of its specific activities, the tax compliance does require specific expertise.

There is an increased scrutiny from the Dutch tax authorities with regard to finance companies (and other tax planning like vehicles). Where a couple of years ago, the low effective tax burden of a finance company was rarely challenged by the tax authorities, nowadays it is quite common that finance companies are closely scrutinized and subjected to extensive tax audits.

For a Dutch finance company in particular the following compliance is relevant:

-

- Registration for tax purposes

- Annual corporate income tax return

- Obtaining tax residency statements (if required)

- VAT returns (if required)

- Dividend withholding tax returns (if required)

We have extensive expertise in the area of finance companies and provide tax compliance services on a professional basis. We are providing tax compliance services to many foreign-based clients.

If you are interested in our services please feel free to contact us via e-mail or to call us at our office on the number +31 (10) 2010466.

We have extensive experience with setting up and maintaining Dutch finance companies. We provide amongst others the following services:

| Advice on setting up a new Dutch finance company/ incorporate a new BV |

| Setting up a finance company/ preparation and filing of the application for the 5% rate |

| Select suitable service providers, like trust companies, lawyers, accoutants, etc. |

| Optimising an existing finance company structure |

| Advice on immigration or emigration issues |

| Obtaining advance tax ruling for financing activities |

| Representation in tax audits |

| Obtaining residence statements |

| Dealing with tax compliance matters |

If you are interested in our services, please feel free to contact us via e-mail or to call us at our office at the number +31 (10) 2010466.