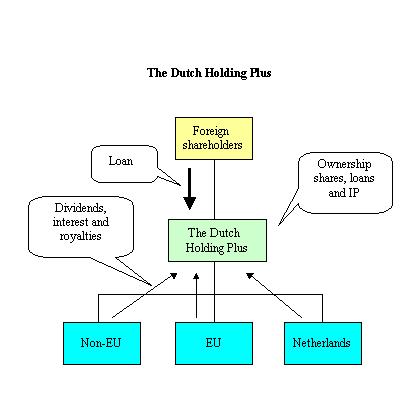

International tax planning - The Dutch holding company plus

During the last couple of years the Dutch holding regime went through a turbulent period. With the latest changes in law per 2007 the Dutch participation exemption regime has been significantly relaxed and the situation has stabilized.

What is left per today is in fact a new sort of holding regime, which apart from a 100% tax exemption for subsidiary income (dividends and capital gains) includes the possibility to shelter other income from taxation. This may in particular be interesting for interest, royalties and service fee income.

The new Dutch holding-plus structure

The changes per 2004 and the latest changes per 1 January 2007

Since 2004 the Dutch holding regime allows a tax deduction of expenses, including interest on acquisition loans.

This means that the Dutch holding company is able to receive tax free dividends and capital gains originating from its (foreign) subsidiaries, whereas at the same time it is allowed to deduct expenses, including interest on funding loans.

In particular the interest deduction is subject to limitations, but in essence the new regime offers the possibility to create tax losses, which can be offset against other sources of income. It is noted however, that limitations exist for the right to carry forward or carry back tax losses.

As from 1 January 2007 the term for carry forward of losses is limited to nine (9) years. The term for carry back is one (1) year.

Since the first of January 2004 limitations apply for the carry forward or carry back of tax losses by holding/financing companies. In essence, the tax losses which originate from a year in which the main activity of the company is the holding of shares or group financing activities may only be carried back or carried forward to tax years in which the company had or has similar activities. Both the nature of the activities and the volume of the activities (balance sheet ratios) are relevant.

Also as from January 1, 2004 a general thin capitalization provision has been introduced. The limitation only applies to interest (and other funding) expenses originating from qualifying intra-group loans. The maximum debt-equity ratio is 3:1, with a general franchise of € 500,000. Special rules apply for calculating the debt-equity ratio.

The ultimate effect of the tax deduction of expenses by a holding company can be that at the Dutch level effectively a very low or no tax at all is due over taxable sources of income, such as interest, royalties and service fee income.

Per 2007 the Dutch participation exemption regime has been further relaxed by abolishment of the general "subject to tax requirement" and the "non-portfolio investment test". Only for subsidiaries which main activity consists of holding portfolio investments or performing group financing services, it is required that they are subject to a tax of at least 10%. Virtually for all other situations, the activities of the subsidiary and the way it is taxed are no longer relevant.

We note that pure foreign real estate companies do in general not qualify as "holding portfolio investments or performing group financing services" so that its shareholders can have full access to the Dutch participation exemption.

As from 2007 the legal form of the Co-operative ("Co-op") has been put on the list of recognized legal entities for the Parent-Subsidiary Directive and the Royalty and Interest Directive. Because the Co-op can be set up in such a way that profit distributions are not qualified as taxable dividends for Dutch tax purposes, the Co-op has become an attractive legal form for an holding company. It is also possible, and highly recommendable, to obtain an advance tax ruling.

Tax benefits at the level of the Dutch Holding-Plus

- Interest expenses on funding loans are within certain limitations tax deductible;

- Dividends and capital gains arising from the ownership of the subsidiaries are tax exempt;

- No Dutch withholding tax on interest paid on the acquisition loan;

- In essence full VAT relief, i.e. refund of VAT on charges to the holding;

- Within the EU:

- dividends can be received free of foreign withholding tax (through application of the Parent-Subsidiary Directive). Strong protection against anti-abuse legislation as a consequence of the substance at the level of holding company (activity test);

- interest and royalties can be received free of foreign withholding tax (through application of the Royalty- Interest Directive). Strong protection against foreign anti-abuse legislation as a consequence of the substance at the level of holding company (activity test) and the fact that the Dutch holding becomes the beneficial owner of the interest and royalty flows.

- Outside the EU:

- the extensive Dutch tax treaty network offers low or zero withholding tax rates for dividends, royalties and interest paid to the Dutch holding;

- the Dutch holding can be allowed an indirect tax credit for the foreign withholding taxes incurred;

- possibility to obtain an advance tax ruling.

We have extensive knowledge an expertise in the area of setting up and maintaining Dutch holding companies and we are gladly prepared to advice you on this subject or to guide you to other professionals who can help you in other specialized areas (like international lawyers, accountants or trust companies).

Our services may include:

| Set up new Dutch holding structure |

| Incorporate BV or acquire shelf company |

| Deal with conversion or immigration issues |

| Clarify the Dutch tax position of existing holding companies |

| Negotiate Dutch tax ruling or provide letter of comfort |

| Advice on tax strategy for the future |

| Deal with Dutch registration formalities and tax compliance matters |

If you are interested in our services, please feel free to contact us via e-mail or to call us at our offices on the number +31 (10) 2010466.